The FPO funds increase is a part of a complete fund-raising plan of round ₹45,000 crore, with stability ₹27,000 crore anticipated to be funded by way of debt. Statements from the Central authorities put up the FPO announcement clearly point out its intentions to make sure a viable pan-India third personal participant within the Indian telecom market. Provided that out of complete debt of ₹2.30 lakh crore (together with optionally convertible debentures), 90 per cent is owed to the Centre, its assertion of help means it is not going to rock the enterprise for the sake of encashing its dues. Therefore the FPO must be considered from two completely different angles – what it means for the enterprise and what it means for the shareholders.

For the enterprise

From over 400 million wi-fi subscribers and market share of round 35 per cent on the time of merger of Vodafone India and Thought Mobile, in 2018, Vodafone Thought’s subscriber rely has declined to 215 million now, with market share at 19.3 per cent. This decline was a consequence of firm’s debt and funding points constraining its skill to spend money on important infrastructure and advertising that was required to develop its 4G enterprise.

This downside will get addressed with the FPO fund increase. Out of ₹18,000 crore, ₹12,750 crore will likely be invested for organising and enlargement of 4g/5g websites, ₹2,175 crore to settle sure deferred funds dues to the DoT, and the remaining for common company functions. The corporate administration is assured that the overall fund increase will likely be enough to compete and develop its enterprise over the subsequent two years. Additional, its present spectrum holdings are enough to develop its 4G enterprise and enough to help migration of 4G subscribers to 5G over the subsequent few years..

Therefore, operationally, the efficiency of Vodafone Thought can enhance, going ahead. Administration can also be betting on enhancing ARPU pushed by two elements — enhance in knowledge subscribers in addition to tariff will increase. With 4G clients at 58 per cent of complete wi-fi subscribers — it’s at 70 per cent for Airtel’s India enterprise and 100 per cent for Reliance Jio — this supplies scope for enhance in ARPU even with out tariff will increase, given the corporate’s new investments are geared to enhancing its 4G buyer base.

At current, ARPU for Vodafone Thought, at ₹145, is properly beneath that of friends’ (Airtel’s at ₹208 and Reliance Jio at ₹182). The corporate has additionally highlighted an attention-grabbing knowledge level in its presentation — within the seven-year interval from September 2016 to September 2023, whereas common wi-fi knowledge consumed/subscriber/month elevated by greater than 8,000 per cent, voice minute utilization/subscriber/month elevated by 160 per cent, blended cell ARPUs in India have elevated solely by 24 per cent. ARPUs in India are amongst the bottom on the earth. Administration believes, given the worth proposition provided by telcos, there’s a robust case for tariffs to extend from right here.

Whereas administration has a degree right here, it must be famous that how a lot the tariffs can enhance will depend upon opponents’ willingness to lift costs in addition to different pressures that will floor. For instance, when there was a cell tariff enhance in 2019, the RBI had famous that it’ll add to inflation. Globally and in India, inflation points haven’t abated. Therefore, with the federal government being a big shareholder in Vodafone Thought (33 per cent, pre-FPO) and largest creditor, it might wish to affect and guarantee a balancing act between the necessity for tariff will increase and controlling inflation.

The corporate additionally plans to develop its b2b enterprise choices. Nonetheless, the income contribution from this phase doesn’t look like important at current.

For the shareholders

Within the bl.portfolio version dated September 10, 2023, we had really useful that traders promote the inventory of Vodafone Thought given our view that there was not a lot elementary upside within the inventory when it was buying and selling at ₹10.50 then. The mid-point of the FPO value band of ₹10-11 is strictly 10.50. Whereas operationally issues will enhance, we aren’t satisfied that FPO value gives worth for shareholders for the next causes:

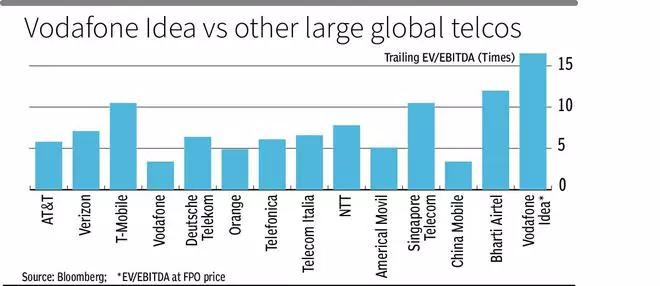

On the FPO value, Vodafone Thought may have a trailing EV/EBITDA of 16.5 occasions, rating it as the most costly giant cell telecom participant globally. Even assuming a really optimistic 20 per cent CAGR in EBITDA over the subsequent two years, it trades at 11.3 occasions CY25 EBITDA.

Bharti Airtel, with a strong stability sheet and well-diversified enterprise, trades at 12 occasions CY23 EBITDA and at 9.5 occasions CY25 EBITDA. Therefore, even below optimistic assumptions, the Vodafone Thought shares at ₹10-11 don’t seem enticing. Additional, traders want to contemplate a number of different overhangs that will loom.

With trailing internet debt/EBITDA at 14 occasions, with authorities help, debt compensation isn’t an issue, however just for some time. Present deferred spectrum cost obligations (DPO) legal responsibility stands at ₹1.3 lakh crore whereas AGR legal responsibility is at ₹65,000 crore, accounting for bulk of the corporate’s debt. A heavy compensation schedule will begin in the direction of the top of FY26. The FPO submitting states that round ₹29,073 will likely be payable in FY26 and ₹43,018/ 12 months payable for every FY from 2027 to 2031, in the direction of DPO and AGR legal responsibility. To know the importance of this, evaluate this with consensus estimates of FY25 income for Vodafone Thought at ₹47,000 crore.

It’s clear the corporate can not generate funds from operations or any asset sale to repay authorities dues. In all possibilities the federal government must help the corporate once more by deferring DPO and AGR cost liabilities from FY26 onwards or convert most of this debt into fairness or optionally convertible debt.

If this debt is transformed into fairness on the FPO value of ₹10, authorities will find yourself proudly owning round 80 per cent of the corporate. If that is transformed into fairness at, let’s say, a value of ₹15/share, it’s going to nonetheless find yourself with a excessive share of round 75 per cent. With full uncertainty on how the debt overhang will likely be addressed, if transformed into fairness – at what value, implications if authorities finally ends up proudly owning an enormous stake and so forth — valuing the shares of Vodafone Thought is a giant train in hypothesis.

Given these, we suggest that traders give the FPO a go and wait and look ahead to now. Borrowing a quote from Warren Buffett, we applaud the endeavour (turning across the firm), however want to skip the trip (for now). Preventing to win seems few years away.

#Vodafone #Thought #FPO #Applaud #Endeavour #Skip #Trip