If one financial institution is working laborious on consolidation submit the mega-merger, there’s a new CEO on the helm in one other who hasn’t laid it down but on the way in which forward for the financial institution. For a couple of extra, there’s a looming query of what subsequent from hereon.

Amidst these questions and issues is IndusInd Financial institution, which comes throughout as a comparatively safer wager with affordable visibility on the way in which forward, whether or not when it comes to progress, high quality of progress or high quality of earnings.

At bl.portfolio, we’ve had a constructive view on the financial institution for over a yr. In end-January 2023, when its valuations have been round 1.6x one-year ahead worth to e-book, we had advisable ‘purchase’ on the inventory. Regardless of 28 per cent appreciation in inventory worth since our earlier advice, the basics supporting the financial institution stay robust and, in truth, could have even marginally improved. Therefore, we proceed to keep up a constructive stance on IndusInd Financial institution inventory.

At ₹1,527 a share, buying and selling at 1.8 one yr ahead worth to e-book, the financial institution is a beautiful decide within the non-public banking house and traders can think about taking recent positions within the inventory with 3 -5 yr funding horizon.

Improved financials

One of many key components binding the constructive view on the inventory is the convincing comeback in financials and return ratios. IndusInd Financial institution has had three dangerous patches — the interval between September 2018 and March 2019 which is the height of IL&FS disaster, round March 2020, when YES Financial institution was positioned underneath moratorium and subsequently in November 2021 following the whistleblower prices on its microfinance operations. FY21 was a deep cleansing interval for the financial institution, particularly with new CEO on board and a few elements of the clean-up continued by means of FY22 as effectively.

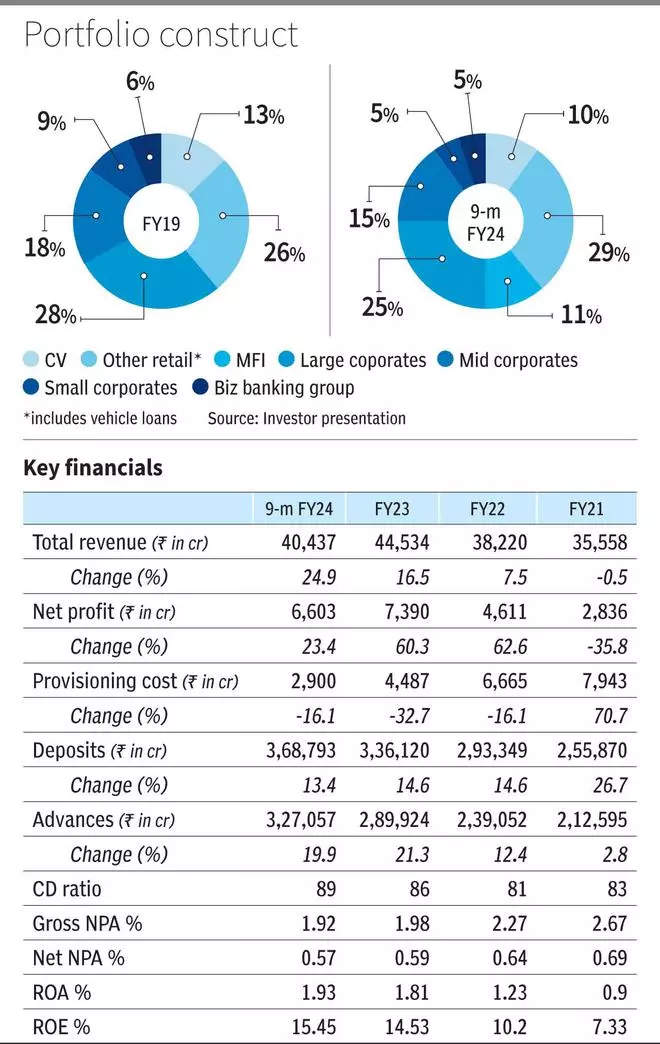

In FY23, IndusInd Financial institution bounced again in full pressure and in an all-round method (see desk). This efficiency has been sustained thus far in FY24.

Planning cycle from FY23–FY26 has guided for progress at 18–23 per cent, enhancing the retail mortgage combine to 55–60 per cent and sustaining pre-provisioning working revenue to loans ratio at 5.25–5.75 per cent. Contemplating the efficiency of the final 4-6 quarters, sustaining this momentum and attaining this technique shouldn’t be a tough process.

Various e-book

Typically the criticism with IndusInd Financial institution is that it’s too commercial-vehicle and MFI-heavy. Whereas MFI will stay an essential piece of the general mortgage e-book at 10 per cent, the granularity which the financial institution is bringing in its automobiles enterprise by rising deal with mid-sized to gentle CVs, vehicles together with used vehicles and two-wheelers, ought to alleviate issues over time. This technique wouldn’t solely foolproof the financial institution from market vagaries however would additionally guarantee sustaining an assured bandwidth of profitability.

IndusInd Financial institution closed Q3 FY24 at 4.3 per cent NIM and has guided for 4.2–4.4 per cent within the medium time period. Compared to friends similar to Kotak Mahindra Financial institution, RBL Financial institution and IDFC First Financial institution (5-6 per cent), whereas IndusInd Financial institution’s NIM could appear smaller, traders must be reassured as a result of this steerage is after factoring for a prudential stance on different unsecured loans (anticipated to be capped at 5 per cent), excluding MFI loans.

Share of unsecured loans within the aforementioned banks is way increased at over 15–60 per cent.

Different plus elements

IndusInd Financial institution has undergone a change in philosophy. From being purely aggressive on progress (which was essential in its preliminary turnaround years of 2008–2018 to place the financial institution on the map), the present stance is to capitalise on pockets the place it has a proper to win.

What this implies is that the financial institution won’t favor to be amongst a crowded consortium of lenders to a big group or venture only for visibility’s sake. Until the financial institution has command over its publicity, together with pricing energy, such a mortgage proposition could also be a no-deal.

Likewise, from CVs being the mainstay within the retail phase earlier, the main target is transferring in direction of automobile financing the place CVs could be part of the general portfolio. Even on the liabilities aspect, the financial institution is evident that deposits ought to feed mortgage progress, which is a departure from its earlier technique of counting on wholesale funding.

This renewed method is guaranteeing that progress is granular, holistic and sticky.

Dangers

With the MFI house evolving sooner than it did a decade in the past, how the financial institution will maintain tempo with competitors with out compromising on high quality can be a key monitorable. The opposite threat is the administration continuity. Sumant Kathpalia has been the CEO of IndusInd Financial institution since March 2020 and is due for reappointment in March 2025.

All eyes can be on whether or not he will get a three-year extension from the Reserve Financial institution of India. That will be crucial, contemplating that Kathpalia is simply half-way within the journey of transformation and his presence is crucial to make sure continuity within the transformation course of.

#IndusInd #Financial institution #Good #Purchase