The corporate is dealing with headwinds in its three sectors owing to aggressive pressures. These pressures might resolve however refrigerant gases division might stay subdued. Whilst growth into new-age options continues to be a chance, excessive progress expectations and better multiples baked into the worth ought to be an opportune time for traders to e-book earnings from the inventory.

Readability on demand pick-up in new growth, regulatory acceptance and total enterprise outlook in Europe is required to take a re-look on the inventory.

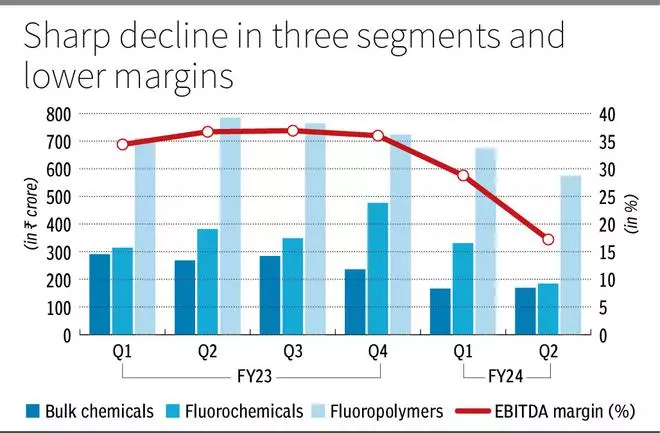

Sector headwinds

GFCL stories three segments: Bulk chemical substances (16 per cent of H1FY24 revenues), Fluorochemicals (Refrigerant gases and specialty chemical substances – 25 per cent) and Fluoropolymers (59 per cent). The three segments reported a major decline in Q2FY24 when revenues declined 37/52/27 per cent YoY respectively and consolidated EBITDA margins contracted by 19 proportion factors to 17 per cent.

The widespread purpose for the three segments’ decline pertains to destocking from purchasers and extra Chinese language provides. Firms/purchasers overstocked provides final 12 months owing to produce chain volatilities. Because the built-up stock is rationalised, demand for chemical substances might be weaker for a couple of extra quarters for all associated firms, not just for GFCL. The speedy rise in rates of interest can also be impacting the price of stock holding, additional pressuring demand.

With Chinese language demand not increasing as anticipated, its home capability of chemical substances can also be discovering its approach to European markets, impacting worth realisations as nicely. GFCL is dealing with quantity decline from destocking and worth decline from Chinese language competitors in latest quarters. It being cyclical in nature, it may be anticipated to reverse as destocking might wane and stock build-up resumes and primarily based on Chinese language financial progress, extra provides could also be curtailed in subsequent few quarters.

Firm headwinds

GFCL additionally faces company-specific points. Refrigerant gases have been to be phased out of manufacturing in US markets steadily. This generated a powerful demand in 2023 earlier than the phase-out. The phase (fluorochemicals) reported a 158 per cent YoY progress in FY23 on sturdy demand and better pricing. Because the demand normalises after stocking and from different markets, the phase will stay subdued, going ahead as nicely. The corporate had deliberate a big capex for R32 refrigerant gasoline, which is on maintain until demand resumption is on the outlook.

Europe, which is the primary marketplace for fluoropolymers, is toying with a ban on polyfluoroalkyl substances or PFAS, except important in nature. GFCL maintains that the long-chain compounds manufactured by it aren’t subjected to the regulation. Additionally, as end-use is into semiconductors, EV and batteries and never in meals grade merchandise, the scope of regulation could also be restricted. Legacy producers in Europe are additionally slicing down on manufacturing in Europe, which is once more driving heightened stocking by purchasers and pushing demand for GFCL’s fluoropolymers down. However this ought to be a short-term strain.

New-age purposes

Although within the midst of a difficult atmosphere, GFCL has a powerful suite of merchandise in improvement, which discover purposes in new-age options. A number of polymers for semiconductors, photo voltaic movies, battery chemical substances and vitality storage have been developed and are in lab evaluation stage with manufacturing capability readied or on the commercialisation stage.

For PVDF (Polyvinylidene fluoride) for electrical car battery, consumer approvals are underway and capability is to be commercialised. Full-scale revenues ought to be anticipated by FY26 on a capability of ₹800 crore and two occasions asset turnover. Equally, purposes for PTFE (Polytetrafluoroethylene), PFA (Perfluoroalkoxy alkanes) and FKM (Fluoroelastomers) are additionally underneath approach, which may open new strains of income supply in subsequent two years. With their being excessive grade polymers with low ranges of impurity and present process consumer approvals, entry barrier might be excessive for competitors to step in when renewables and inexperienced vitality options come into focus.

Financials and valuation

Consensus estimates are factoring within the present negatives and likewise a pointy restoration. The FY24 estimates are baking in 22/55 per cent decline in FY24 for income and earnings (22/62 per cent YoY decline reported by H2FY24). Owing to commercialisation of recent services and cyclical restoration in base enterprise, the FY25 estimates are at 27/67 per cent YoY progress in income and earnings.

Not solely is a pointy restoration anticipated, however the market can also be valuing such progress at 40 occasions earnings in FY25. This leaves little room for error; dangers from extreme regulatory rulings, execution dangers in new services, failure of China to soak up its chemical manufacturing and international progress outlook aren’t priced into the dangers. With the latest rally of 28 per cent in final six months, traders can e-book earnings from the inventory.

Why

Excessive consensus estimates and excessive valuation

Readability on regulation and demand outlook wanted

Sturdy run in latest durations

#Buyers #Guide #Income #Gujarat #Fluorochem