Right here’s a take a look at some components that may show you how to resolve whether or not you want a big cowl.

Premium distinction may be tempting

The premiums for a ₹1-crore cowl might tempt you to go for it. On a mean, for a 30-year-old male with no pre-existing circumstances, a ₹5 lakh/20 lakh/1 crore well being cowl will value ₹7,791/12,775/20,100 each year respectively (common of fifteen main insurance coverage suppliers). The bang for buck is clearly evident with solely a 50-60 per cent improve in premiums throughout the classes for a 300-400 per cent improve in cowl. On a normalised foundation, throughout insurance coverage suppliers, a ₹5-lakh cowl could be accessible at ₹16 per ₹1,000 of canopy, ₹6 per ₹1,000 of canopy in ₹20-lakh class and ₹2 per ₹1,000 cowl within the ₹1-crore class. The pricing implication means that the first threat is that of being admitted for medical care. Past this, the uncommon threat of an outsized declare is a manageable occasion and therefore not priced proportionally.

.jpg)

Policyholders might select to give attention to growing their cowl, however the over 50 per cent improve in annual premium (that comes with ₹5 lakh to ₹20 lakh or to ₹1 crore) also needs to be saved in thoughts. As prices are sure and well being claims are sporadic, the probability of outsized well being claims is uncommon, not less than going by a standard distribution. As a substitute, personalised wants and affordability of premiums over the following twenty years ought to be factored into the acquisition consideration. Additionally, premiums are inflationary over longer intervals and improve additional on change in well being circumstances. In such a case, beginning off from an simply reasonably priced protection and including acceptable riders alongside the best way could also be helpful in comparison with starting with a bang.

Present cowl may be enhanced

Earlier than contemplating the next cowl, one ought to exhaustively look to stretch decrease ranged covers. The choices accessible can shock policyholders. Present covers are enhanced by 100-200 per cent by way of choices reminiscent of restoration of canopy and No Declare Bonus (NCB) at no extra value (near-standard within the trade). Even larger improve may be achieved by buying top-up/super-top up riders. Restoration of canopy refills the well being cowl in any given 12 months if a previous declare had depleted it. The probabilities of assembly a second declare in a 12 months (usually to the extent of authentic sum insured) for an unrelated sickness (w.r.t to sickness in first declare) are improved with this characteristic.

Niva Bupa, SBI Normal, Star Well being, Chola MS and Manipal Cigna cowl associated sickness as nicely. The NCB characteristic step by step will increase bonus cowl to match the unique cowl. The unique cowl is doubled in Manipal Cigna’s case and is moved up by 50 per cent with New India Assurance. The speed of doubling the duvet with NCB may be gradual (over 10 years) or quick (inside three years) however so would be the tempo of retreat on making a declare in any 12 months. Basically, over 5 years, one can not less than double one’s cowl at no extra value utilizing restoration of canopy and NCB.

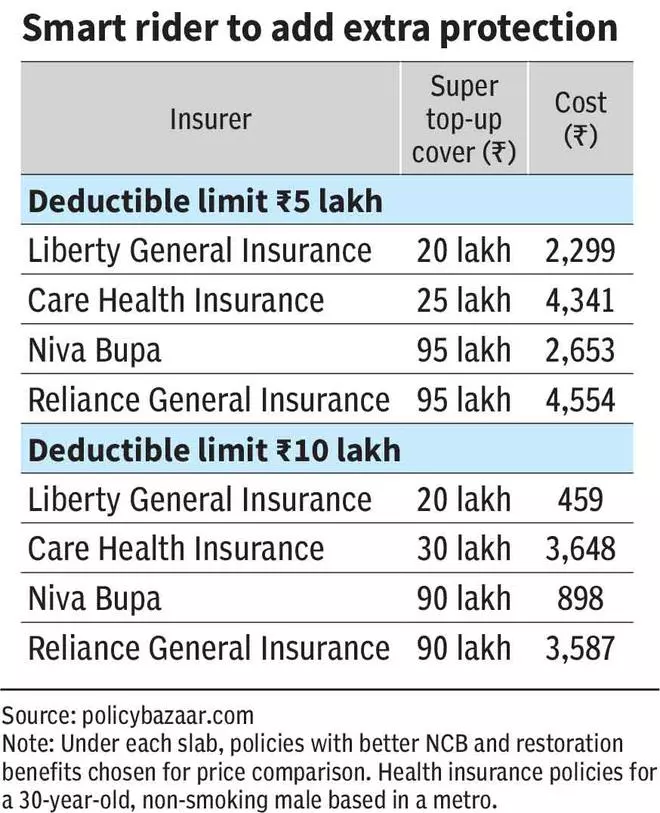

High-up/super-top up riders bought moreover over the bottom coverage kick in when the pre-decided deductible restrict (declare quantity paid by the policyholder or base coverage cowl) is breached. The truth is, some insurance coverage suppliers are that includes this selection (₹5/10 lakh in base coverage + ₹90/95 lakh in tremendous top-up as an alternative choice to their very own ₹1-crore covers — Aditya Birla and Niva Bupa, as an illustration. In comparison with an outright ₹1-crore buy, which prices round ₹22,000 for a 30-year-old male, this selection is cheaper at ₹9,500 at Aditya Birla. Alternatively, one may purchase a ₹5-lakh cowl for ₹8,500 and add a super-top-up of ₹95 lakh with a deductible restrict of ₹5 lakh for a complete premium of ₹10,500.

Essential sickness rider can also be one other type of protecting high-cost procedures. The rider may be bought to supply a lump sum quantity (starting from ₹10 lakh to ₹1 crore) on the prognosis of a vital sickness (20 to 60 illnesses lined). This supplies an alternative choice to shopping for a big well being cowl if the first concern is to cowl these indications.

Options for larger covers not distinctive

The distinction between a ₹5-lakh and a ₹1-crore well being cowl is actually within the inpatient value cowl. One can’t anticipate decrease ready intervals for pre-existing ailments or larger sub-limits with the next cowl. The fundamental product and the vital options (day care process record, NCB and restoration of canopy) are frequent throughout larger or decrease ranges of covers. The truth is, in terms of room limits, even a ₹5-lakh cowl gives single personal AC room in most insurance policies. Solely New India Assurance has a room hire restrict of ₹5,000 with its r ₹5-lakh well being cowl.

Nonetheless, a ₹1-crore coverage may also help in some methods. As an example, cataract surgical procedure sub-limit is positioned at 20 per cent (higher restrict of ₹1 lakh) in Bajaj Allianz, which could result in some out-of-pocket prices when claimed with a ₹5-lakh cowl. Equally, unintentional loss of life profit matches sum insured at Star Well being, implying the next unintentional loss of life profit can solely be met with the next cowl. Whereas single personal AC room is the restrict in HDFC’s medical health insurance, the restrict for covers above ₹50 lakh is eliminated. With another high-value insurance policies, OPD covers, dental advantages, free check-ups may enhance for larger covers.

Contemplating the price of therapies overseas, international protection makes higher sense when well being cowl is larger. On this regard, TATA AIG Medicare plan permits for reimbursement of inpatient remedy value overseas if the prognosis is made in India (in comparison with solely worldwide emergency remedy cowl throughout different insurance policies).

How a lot cowl?

So, given the components mentioned above, how a lot cowl is good? Whereas medical remedy prices and the inflation in the identical, 12 months after 12 months, may be an indicator, the appropriate well being cowl is in the end a personalised choice. Components that nudge the policyholder to take the required cowl larger or decrease embrace medical histories in addition to current insurance coverage back-up with employers, as an illustration. After weighing these components, the well being cowl and the way a lot you spend on the premiums mustn’t chase excessive outlier dangers at the price of affordability and therefore, continuity of the coverage.

Whereas well being dangers are frequent for all, dangers flagged in household medical histories, particularly these being tackled by trendy science or the most recent applied sciences, name for the next cowl. Amongst these are immunological and oncological circumstances. Breast, lung or ovarian most cancers might have been a loss of life knell up to now however with medical advances, they now carry a restoration prognosis. However they arrive at a excessive value of remedy and so do liver or kidney transplant procedures at ₹10-25 lakh in comparison with persistent circumstances of cardiac, bronchial asthma, dialysis and even diabetes that carry a invoice of ₹3-10 lakh on the larger finish. Evaluate this with the typical hospital invoice of ₹2 lakh per admission (Common income per working mattress * Common size of keep) at main hospitals.

The prevailing insurance coverage offered by employers or State/Central organisations can mood the necessity for larger covers. However it is usually a trade-off between your selecting to maneuver out to an organisation the place well being cowl could also be decrease or not offered or, say, turning into an entrepreneur the place you’ll not have the security internet of a bunch well being cowl.

Do larger covers make sense for household floaters?

Household floater coverage covers relations underneath one sum insured with a unified premium fee. There may be scope to carve the well being cowl for every particular person in a household plan however leaving it open for all could also be helpful. Whereas choosing a household floater, the next sum insured appears to be an computerized selection for a lot of, the reason is that many people are lined. Nonetheless, a number of relations needing medical care concurrently in a single 12 months remains to be a low likelihood occasion. However for peace of thoughts, the next cowl is mostly chosen in household floaters.

On a value foundation, a household floater is clearly cheaper than three or 4 particular person insurance policies and the paperwork concerned will probably be a lot lighter. Evaluating particular person and household floater insurance policies, for a ₹20-lakh cowl from ten insurance coverage suppliers, the typical household floater premium comes at ₹25,000 each year (Dad and mom aged 35-30 and youngsters aged 4 and 6). That is double the premium of a person plan for every of them. For a similar household, a ₹1-crore coverage will probably be at a mean ₹41,000 among the many 10 insurers.

A decrease, ₹5-lakh cowl for the household is priced at ₹15,000. NCB and restoration of covers are much like particular person plans, permitting for close to doubling of canopy on claim-free first few years. The tremendous top-up plans to boost this cowl can be found from ₹6,000 to ₹11,500 for a ₹95-lakh cowl and ₹5-lakh deductible restrict.

Household floaters for the aged (kids and fogeys above 60 years) proceed to stay costly (ranging from ₹45,000 for a ₹5-lakh cowl). They could additionally want larger underwriting requirements, together with medical analysis for coverage initiation. Additionally, contemplating the next medical care requirement for elders, it could be prudent to decide on particular person plans for the aged.

#leap #1crore #well being #covers