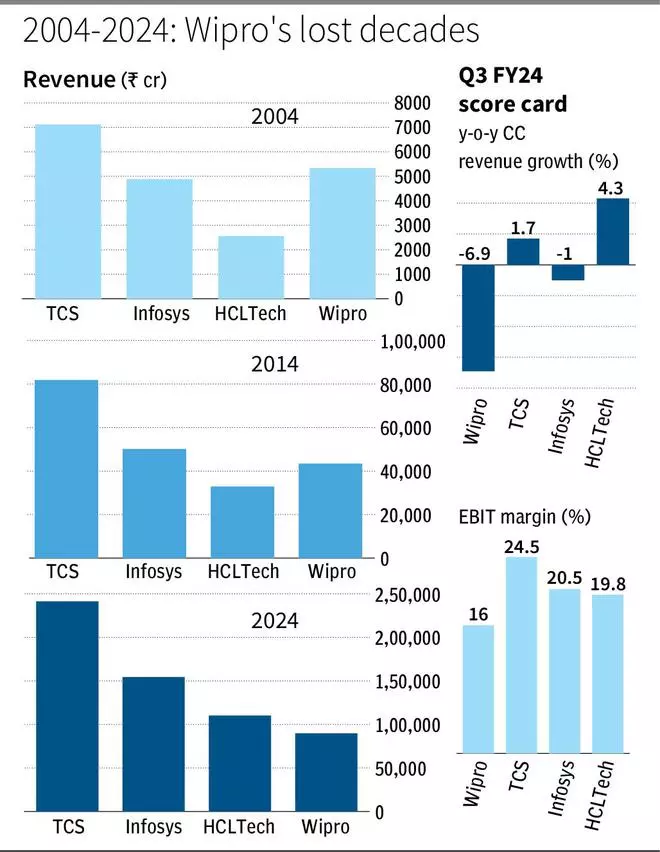

Quick-forward to at present and when you think about FY24 revenues (9M actuals + 4Q estimates), Wipro’s income is 63/42/18 per cent decrease than that of TCS, Infosys and HCLTech.

Nothing can extra clearly clarify how a lot the corporate has fallen behind within the final 20 years because it tried a number of fixes and techniques for the reason that time its high-profile CEO, Vivek Paul, unexpectedly stop in 2005. Whereas the optimistic momentum did stick with it for a number of extra years, it didn’t final too lengthy. That it stays amongst the massive 4 in Indian IT even after being such a laggard during the last 20 years is extra a mirrored image of how large and outstanding it was prior to now.

Turnaround hope fades

Three-four years again, hopes had been renewed when the corporate indicated clear intent to return to its previous aggressive method that made it so pre-eminent. Chairman Rishad Premji said that one will see a ‘bolder Wipro’ that will not be afraid to upset the apple cart. The appointment of Thierry Delaporte in 2020 and his strategic plan was well-received by the market. It did begin off properly with Wipro leads to FY21 and most of FY22 displaying renewed development comparable with friends, however doubts began creeping in after efficiency began waning once more in FY23 and FY24. The turnaround hopes have now come a full circle with the latest announcement that Delaporte is resigning with quick impact.

At bl.portfolio, we had really useful a ‘e-book revenue’ on Wipro three years again in our version dated Might 23, 2021, when the inventory was buying and selling at 513. At the moment, our view was that risk-reward within the inventory was fully unfavourable as valuations (premium of 72 per cent to 10-year common then) mirrored full confidence in everlasting turnaround in Wipro’s prospects, whereas challenges nonetheless remained. Since then, the inventory is down by 7 per cent whereas the Nifty is up by somewhat over 60 per cent, reflecting important underperformance by Wipro on an absolute in addition to relative foundation within the final three years.

What ought to traders do now amidst administration rejig? The inventory at the moment trades at a one-year ahead PE of 20 occasions now, cheaper versus 25 occasions in Might 2021. Nonetheless, Wipro has but once more develop into a ‘present me’ story. Threat-reward stays unfavourable even at PE of 20 occasions, given its final 10 and 5-year web earnings CAGR are lacklustre at simply 4 and 6 per cent. EPS CAGR, juiced by buybacks, is barely higher at 6 and seven per cent, however nonetheless weak.

Whereas newly appointed CEO, Srinivas Pallia is a Wipro veteran (three a long time within the firm and a number of management roles) and comes with sturdy credentials, given the final 20 years of underperformance of the corporate, traders should ideally stay up for proof of turnaround. Thierry Delaoporte’s abrupt exit and previous management points at Wipro are validation of the truth that enterprise turnarounds are difficult and traders must weigh the chance versus reward earlier than inserting their bets.

Additional, the macro financial backdrop for IT companies corporations stays hazy, with inflation re-accelerating once more within the US and expectations for rate of interest cuts for the 12 months getting pared again. It will solely make a turnaround much more difficult for Wipro. Given these elements, we preserve a promote suggestion on the inventory for now.

Current efficiency

In a difficult Q3FY24 for the IT companies business, Wipro continued to underperform. Its Y-o-Y fixed foreign money income development was very weak at -6.9 per cent though marginally higher than expectations. Working margin at 16 per cent was 40 bps forward of consensus expectations, and working earnings was 3 per cent above. Markets overreacted to outcomes by deciphering it as a sign that enterprise development had bottomed out and the inventory moved up by 20 per cent in a four-week interval after the outcomes. It has nonetheless given up many of the good points since.

Wanting into the main points, it was clear the outcomes didn’t give a lot to be optimistic about and enterprise challenges stay. Except for Healthcare vertical, all verticals reported flattish to declining efficiency Y-o-Y and Q-o-Q. Main vertical BFSI, which accounts for 33 per cent of income, was down by 4.9 per cent Y-o-Y.

A number of the optimism within the inventory submit the outcomes was on expectations that there could also be some restoration in BFSI. Nonetheless, given latest unfavourable inflation information within the US (Wipro derives near 60 per cent of income from North America), larger rates of interest and a few turbulence for the BFSI sector in North America may proceed for some extra time. Accenture’s up to date FY24 outlook reported in March, which mirrored enhanced readability on CY24 IT budgets of shoppers, indicated that weak spot in IT companies could final by way of CY24.

Additional, it’s unlikely that Delaporte would have stop if developments had bottomed in 3QFY24, as he would have been greatest positioned to steer by way of the restoration part as properly and one wouldn’t wish to rock the boat at such a juncture.

Therefore, Wipro will seemingly undergo a reset part beneath the brand new CEO within the midst of an unfavourable macro backdrop. Whereas one can positively be hopeful of a turnaround, it is going to be long-drawn; and the inventory is unattractive at present ranges.

#Wipro #Present #Story